In times of a sold-out real estate market, when there are multiple buyers for each property, those with money to spare often get priority. Some banks have responded to this need with a special mortgage product.

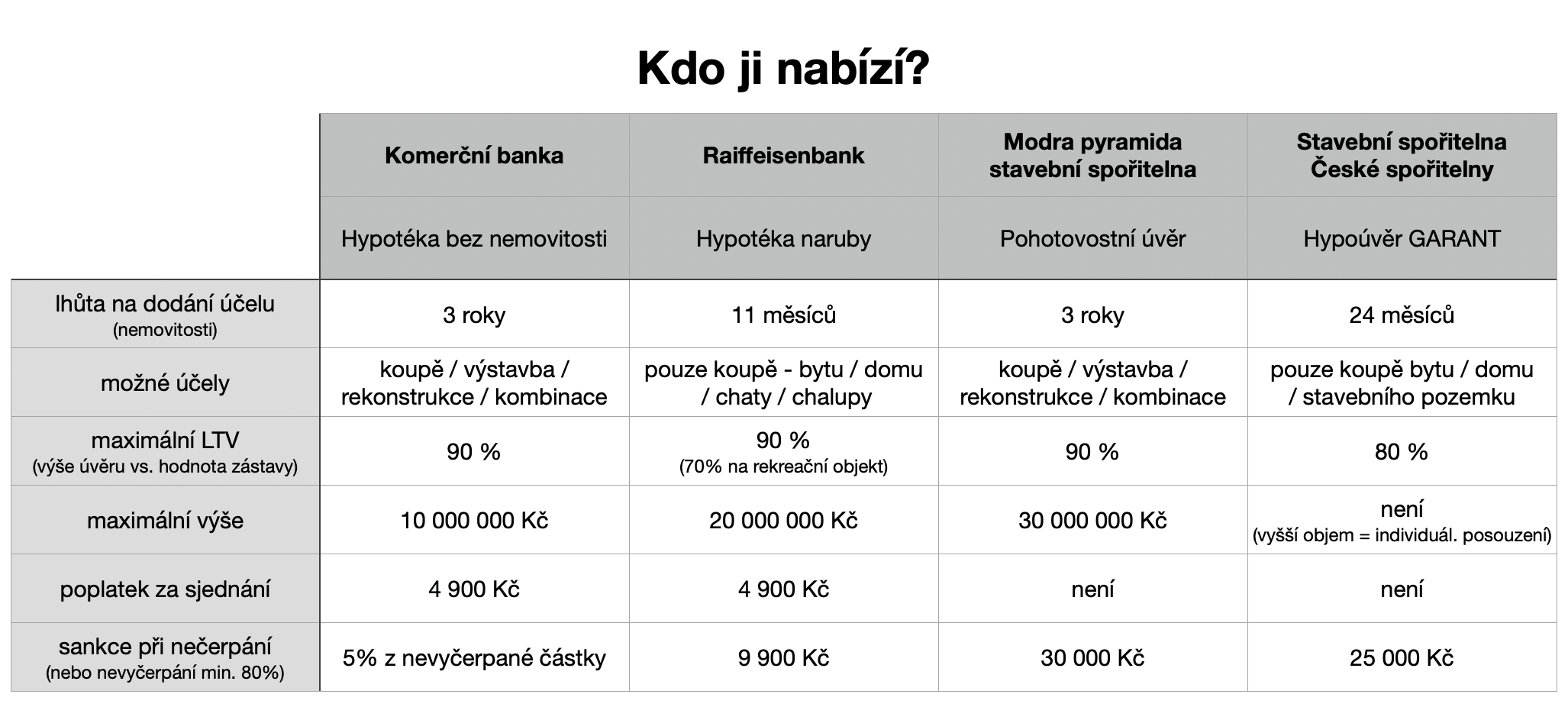

Mortgage without property, Mortgage inside out, Mortgage GARANT, Standby loan – these are the names of mortgage products that basically provide the same service.

This consists in providing the bank with documents to prove your ability to repay the mortgage and the loan is then approved only on the basis of these documents. In practice, you provide the bank with proof of income from your employment or tax returns and bank statements and tell them how much mortgage you would like. If the numbers match, the loan is approved in a few days and you can sign. Then you just deliver the property at the given time and live in it. It sounds simple and if everything works out as it should, this product can serve you well. However, it is not always a good idea to rush into such a mortgage. I’d almost say there are more cases where it’s not a good fit. So let’s break it down further.

What is it for?

The main purpose of this specialty is to provide security in the form of an approved mortgage. This comes in handy when you are looking for a property and you want to be the one who has the money ready and can react quickly to the offer and sign the reservation contract in peace.

If you know what you are looking for, know how much, have your own funds ready or another property to secure, then you are probably the ideal candidate for a mortgage without a property.