Probably no one who has been interested in the possibility of taking out a mortgage in recent months could have missed the various alarmist reports about rising mortgage interest rates.

However, the average interest rate on mortgages in the first quarter of 2021 was still below 2% p.a. However, this is mainly due to the fact that the signed loans were arranged earlier and therefore at a time of lower rates.

At the moment we are practically out of rates starting with one. New mortgages start at 2.XX% and banks continue to plan to increase.

What it means in real numbers

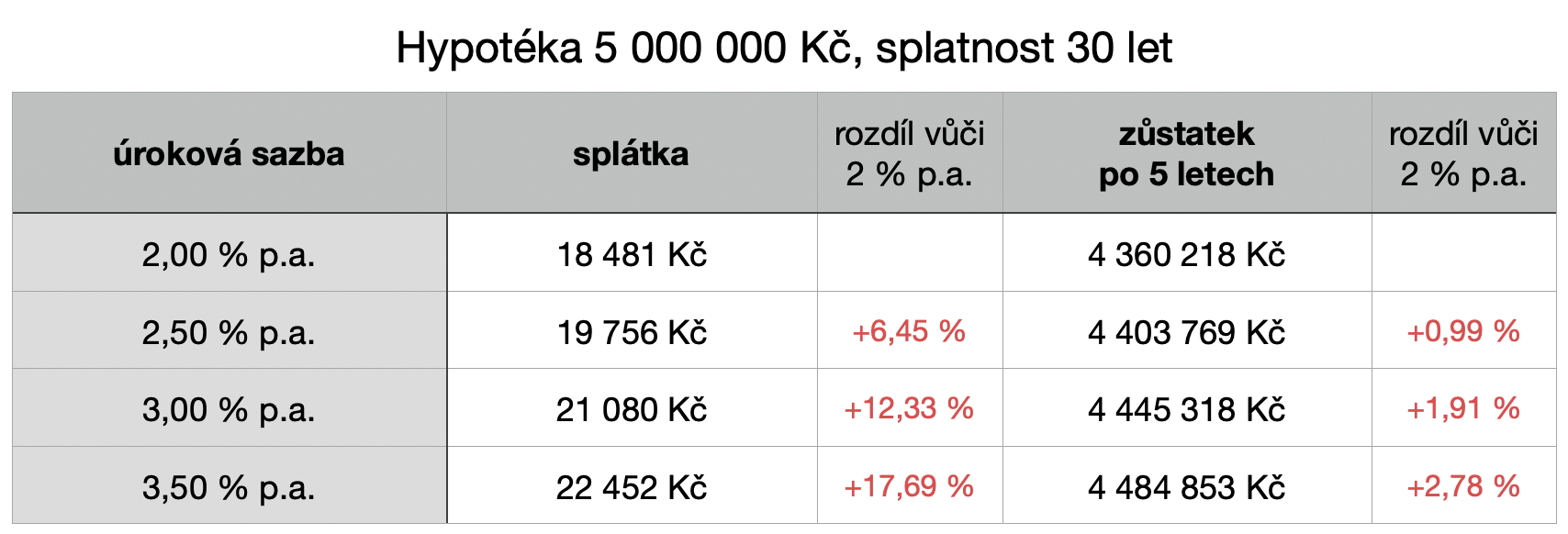

So let’s see what a higher interest rate will do to your repayment and how it will affect your loan balance over the years. An example would be a mortgage for 5 mil. CZK and a maturity of 30 years.

The table shows that the interest rate primarily affects the amount of the repayment and only minimally affects the balance.

What happens after fixation

If you have already arranged your cheap mortgage, then you are assured of the amount of your repayment for the duration of the fixation period. What happens next? The bank sends a letter 3 months before the end of the fixation period with an offer for a new fixation period. At this point, it should be noted that it is almost always possible to reduce this offer, either by proper negotiation with the current bank or by switching to another bank. In either case, it is advisable to contact a financial advisor who will have some negotiating leverage.

However, if you have a mortgage at 2% and at the end of the 5-year fixation the market rates will be around 3%, then we will not be able to avoid the increase. Below we show what such an increase in the interest rate after fixing can mean in real terms. I consider it important in this case to take into account a healthy inflation rate (2% per year), i.e. to express any increase in “today’s money“.

The possibility of increasing the repayment after fixation should be taken into account and not take out a mortgage with a repayment at the edge of your financial possibilities. On the other hand, even in a very pessimistic scenario, we are talking about an increase of a tenth in real money, which is not so scary if we consider that wages have risen by 26% in total over the last 5 years. If you are still afraid of the possibility of an increase, choose a longer fixation (e.g. 8-10 years), which is slightly more expensive but represents the desired security.